Fixed Indexed Annuity 101

Got Questions? Need Answers Fast? 👉

Overview

There is a lot of "meat on the Bone" here

What a Fixed Indexed Annuity Is NOT?

A Fixed Indexed Annuity (FIA for short) is not a variable annuity. There is no direct market exposure and no risk of losing principal due to market declines. It is not an investment or a security. You are not buying stocks, mutual funds, or participating directly in the market. An FIA is not built for short-term gains or quick returns. FIAs are not for timing the market or generating immediate upside. It is not designed to match full market returns. Because of caps, spreads, or participation rates, you trade some upside potential in exchange for downside protection (0% floor) (Will Explain these Terms Below). It is not a CD. CDs and MYGAs (Multi-Year Guaranteed Annuities) offer fixed, contractual interest rates each year. An FIA does not guarantee annual interest for the contract term and your return depends on index performance, within defined limits.

What a Fixed Indexed Annuity IS?

A fixed indexed annuity (FIA) is a contract with an insurance company designed to help you protect your principal, grow tax-deferred, and/or create guaranteed income for life. An FIA has two accounts, A fixed account and an indexed account that you can allocate funds towards. The insurance company credits interest based in part on the movement of a market index (like the S&P 500®) while protecting you from market losses when held according to the contract terms. Below we will dive deeper into fixed indexed annuities.

Features of Fixed Indexed Annuities

As a result of the way in which interest is credited to equity indexed annuities, these products are characterized by a number of unique features. For example, most include some provision that limits the amount of indexed interest that will be credited to the contract. These limits take the form of participation rates, margin, triggers and caps. Indexed annuities are a form of fixed annuity. However, the interest credited to the contract is not declared in advance by the insurer; instead, it is based on the performance of an independent market index, such as the S&P 500. For example, if, the index to which Index Annuity ABC is tied was at 1000 when the contract’s interest crediting period began and reached 1100 when the crediting period ended, the index increased by 10 percent [(1100 - 1000 = 100) ÷ 1000]. Consequently, the basis for the interest that will be credited to Index Annuity ABC for that period is 10 percent. In this way, indexed annuities allow some measure of participation in market-based returns: the increase (or decrease) in the index to which the product is tied is the basis for the amount of interest that will be credited.

Minimum Guaranteed Interest Rate

Indexed annuities also provide for a minimum guaranteed interest rate, which protects the values in the contract against market downturns. At the end of each interest crediting term, the indexed interest or the minimum guaranteed rate, whichever is greater, will be credited to the contract. In this way, an indexed annuity buyer’s principal is protected from loss. However, the guaranteed minimum rate for an indexed annuity may be lower than the guaranteed minimum rate that applies to a traditional fixed annuity, and it is common for indexed annuity insurers to apply the guaranteed minimum rate to only a portion of invested premiums, such as 87.5 or 90 percent.

Participation Rate

The participation rate, also know as par, is the amount or level of the index increase that will be credited to the contract. For example, if the participation rate is 80 percent and the index to which the contract is tied increased by 11 percent over the crediting period, then the contract will be credited with 8.8 percent interest (.80 × .11 = .088). If the participation rate is 70 percent and the index to which the contract is tied increased by 11 percent over the crediting period, then the contract will be credited with 7.7 percent interest (.70 × .11 = .077).

Indexed annuity participation rates vary widely from insurer to insurer and from product to product. Some may be as low as 50 percent; others may be as high as 90 percent or 100 percent. Products with lower participation rates may feature additional benefits that are not included on products that apply higher participation rates. Conversely, products that have longer terms may carry higher participation rates than those with shorter terms.

Margin

As an alternative to—or in addition to—a participation rate, some indexed annuity issuers use a margin (or spread) to determine the interest rate that will be credited to their contracts. A margin is a stated percentage deducted from the percentage change in the index level before that percentage is applied as an interest rate to the annuity funds. Thus, a margin is subtracted from the index yield, and the remainder is the credited interest rate. For example, if the index which the contract is tied increased by 8 percent and the margin is set at 5 percent, the interest rate that will be applied to the annuity for that specific crediting period is 3 percent (.08 - .05 = .03).

Cap

In addition to a participation rate or margin, indexed annuities usually impose a cap, which is the maximum amount of interest that will be credited during any one interest crediting period. An 8 percent cap, for instance, limits the amount of interest credited to the contract in any interest crediting period to 8 percent regardless of the performance of the underlying index and regardless of the participation or margin rates.

Floor

Most indexed annuities contain provisions that prevent any negative index return from affecting the contract’s previously credited values. This is known as the floor: the minimum amount of indexed linked interest that is to be credited to a contract during any crediting period. With most indexed annuities, the floor is zero. In other words, if the index to which an annuity is tied were to decrease over the crediting period, the amount of indexed interest that would be credited to the contract would be zero no indexed interest would be credited. As a result, a decline in the index would not equate to negative interest crediting.

Trigger

A trigger strategy is one of the simplest ways your money can grow inside a Fixed Indexed Annuity (FIA). Instead of tracking every move of the market, a trigger focuses on one question: Did the index finish higher than where it started? At the beginning of your contract term (typically 1 year), your annuity is linked to a market index like the S&P 500 and assigned a "trigger" or preset interest rate. For example, 7%. If the index goes up at all, you receive the trigger rate of 7%. If the index is flat or down, you receive 0%. Your principal is never reduced due to market loss

Example

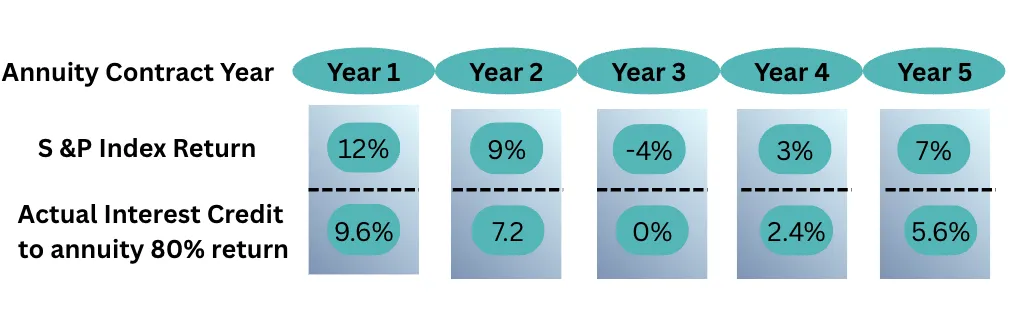

Here is an example. Lets assume that an indexed annuity provides for annual interest crediting, an 80 percent participation rate, and a zero percent floor. During the first two contract years, the index to which the annuity is tied yields a positive return; the third year, the index return is negative; in years four and five, the returns are again positive. The following illustrates the amount of interest that would be credited to the contract in each of these five years:

The negative index return in Year 3 does not generate negative interest crediting; instead, the zero percent floor results in no index interest credited in Year 3, and the annuity’s value does not decline.

An indexed annuity’s floor should not be confused with the product’s minimum guaranteed rate of return. The floor represents the minimum rate of indexed interest that will be credited to the contract during any crediting period; the minimum guaranteed rate of return is the rate that will be applied to the contract at the end of the contract’s crediting term if the index interest accumulations are less than the minimum guaranteed.

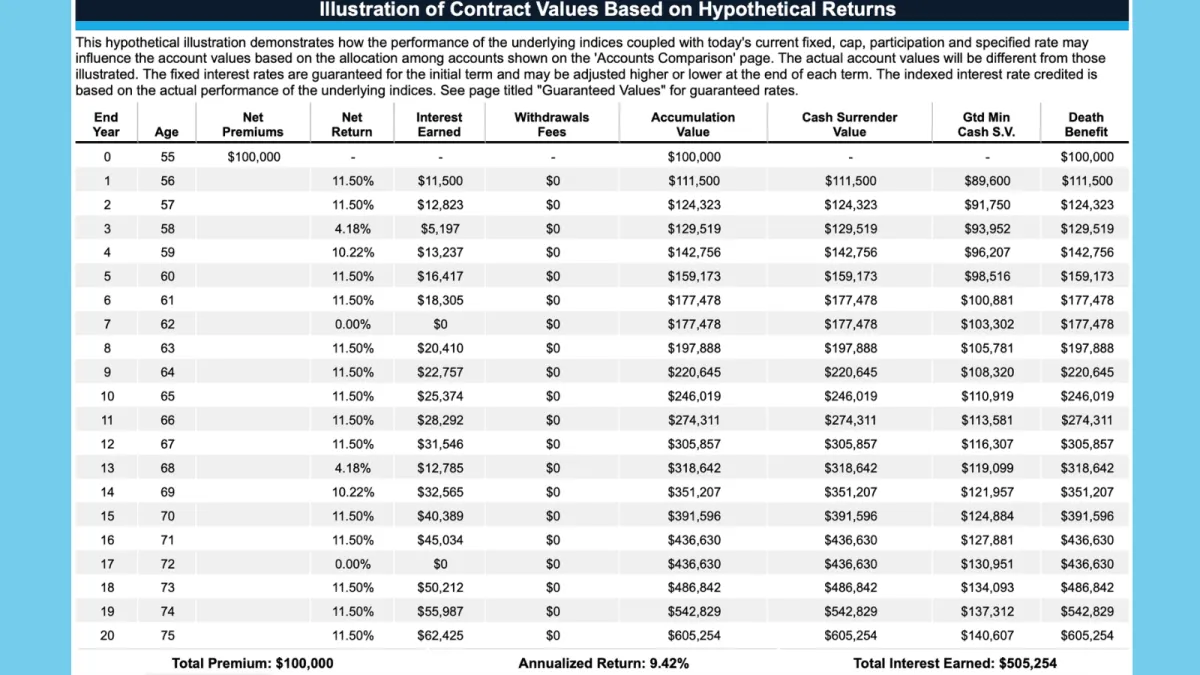

Below is a sample illustration we provide to clients, outlining the potential future performance of a Fixed Indexed Annuity based on current assumptions.

How a Fixed Indexed Annuity Works—Step by Step

Most retirees appreciate FIAs once they see the “plumbing.” Here is the basic flow from the moment you start a contract through the income phase.

Important: Every annuity is different. Rates, caps, riders, surrender schedules, and guarantees vary by insurer and by contract. Always review the actual product disclosure, not just a brochure.

Annuity Gal presents Annuity options

Find the Annuity best for your needs and goals

Sign contract from Annuity Gal with Insurance carrier

Fund your account(s) insurance carrier

Watch your money grow daily, weekly, monthly or yearly

Retire and preserve wealth or guaranteed income

The Quick Breakdown

1. You pick your goal:

- Preservation : protect principal from market losses and aim for steady, capped/index-linked interest with highest return.

- Income: build a future guaranteed lifetime income stream (often later), while still protecting principal from market losses.

2. You decide how much money:

Provide us with the dollar amount you plan to fund the annuity with. Most insurance annuity contracts start with a minimum of $10,000 but this varys.

2. You pick your timeline

Your time horizon (3 / 5 / 7 / 10 years) aka Surrender Period. This is the commitment window where early large withdrawals may trigger surrender charges.

3. Choose how you plan to fund

Qualified funds (IRA/401k rollover): tax-deferred already;

Non-qualified funds (after-tax money): growth is tax-deferred; taxation is generally on the gains portion when withdrawn.

4. We'll review your annuity options

We show you a short list of top-fit FIAs based on:

How much liquidity you need, Whether income is “now” vs “later”,

Risk tolerance (more conservative vs more crediting potential)

5. Fill out application and suitability questionnaire

Every insurance company has a seperate application. We will walk you through any part or all of the process. Then we submit it to the carrier.

Most contracts still allow penalty-free withdrawals up to a limit each year (varies by carrier/contract). You allocate to index strategies or fixed account on the application.

6. Fund your account!

You can fund an annuity by wire, check, rollover, transfer, or exchange. Most people use a check or a direct rollover from retirement accounts. If speed matters, we use a wire.

7. Throughout the contract term

If it’s a preservation/growth annuity, you generally let it compound, only access if needed.

If it’s an income annuity, turn your income on and take withdrawals based your contracted terms .

8. End of surrender term / contract year

You keep, move, or reset

At the end of the term, you can:

Keep it (often renew into new terms)

1035 exchange (non-qualified) or rollover (qualified) to another annuity

Start/adjust income depending on the contract

Notes

Your money is not directly invested in the stock market.

You select crediting strategies tied to an index (e.g., S&P 500).

Your interest credit is typically governed by a cap, participation rate, or spread.

Interest Crediting

Interest credits are calculated on a schedule

On each crediting term (commonly 1–2 years), your contract:

-Tracks index performance for that term

-Applies the contract’s cap/participation/spread

-Locks in any credited interest

-If the index is negative for the term, you get 0% for that term, never a loss

-You manage liquidity and withdrawals

Key point: the income account value used to calculate income is often different from the actual account value you could cash out.

A Core Benefit

Creating Income You Can’t Outlive

Running out of money is the #1 fear many retirees share. Fixed indexed annuities can convert part of your savings into a dependable paycheck—backed by the issuing insurance company—that continues as long as you live, and in many cases, as long as your spouse lives as well.

Common Income Options

- Lifetime income rider: For an additional fee, many FIAs offer a rider that grows a separate income value and guarantees payments for life, even if your account value goes to zero.

- Single or joint life payments: You can often choose to cover just your life or both you and a spouse.

- Period certain payouts: Income guaranteed for a set number of years (for example, 10 or 20), whether you live that entire period or not.

- Flexible withdrawals: Some contracts allow systematic withdrawals instead of a formal annuitization, within specific limits.

How Much Income Could You Expect?

Income amounts depend on:

- Your age when income begins

- Whether payments are single or joint life

- Current interest rate environment

- How long your money has been in the contract

- Whether you added an income rider and its rules

A personalized illustration can show how much lifetime income a specific FIA may provide in your situation. Requesting quotes from multiple highly rated insurers can help you compare options and avoid overpaying in fees.

Pros of Using an FIA for Income

- Can help cover essential expenses (housing, food, healthcare).

- Reduces pressure to chase risky market returns in retirement.

- Can complement Social Security and pensions for a stronger income floor.

- May include benefits for a surviving spouse.

Another Core Benefit

Preserving What You’ve Worked a Lifetime to Build

When you are already retired—or very close—large market losses hurt more. You may not have decades to recover. FIAs are built to prioritize principal protection (subject to the claims-paying ability of the insurer and the terms of the contract) while still offering a chance for growth.

Principal Protection in Plain English

- Your money is not directly invested in the stock market.

- When the index is negative, your account value is not reduced due to index performance (you may receive 0% interest for that period).

- The insurance company backs the guarantees; your risk is tied to their financial strength and the contract terms, not to daily stock prices.

- You must still respect surrender charges and contractual rules to avoid penalties.

FIAs vs. Keeping Everything in the Market

- Market-only approach: Offers high growth potential but exposes you to full downside risk, sequence‑of‑returns risk, and behavioral mistakes during volatility.

- FIA approach: Trades some upside potential for insulation from market losses and the option for guaranteed income.

- Many retirees use FIAs to cover essential expenses, while leaving other assets more growth‑oriented.

- The right mix depends on your risk tolerance, health, other income sources, and legacy goals.

What About Leaving Money to Heirs?

Most FIAs allow a named beneficiary to receive any remaining contract value when you pass away—often without going through probate. Some riders and contract options can enhance or shape what goes to your heirs, while others prioritize maximizing lifetime income instead.

A careful review can clarify how much of your annuity is meant for you (income and safety) versus how much is meant for your legacy.

Costs, Surrender Charges, and Real‑World Risks

FIAs are not magic. They have trade‑offs and must be used carefully. Knowing where the costs and risks show up helps you ask better questions before you sign anything.

Good fit: Long‑term, conservative savers who can commit funds for the full surrender schedule.

Poor fit: People who may need the money back quickly or who are primarily seeking aggressive market‑like returns.

Where Costs Typically Show Up

- Income riders: Often have an explicit annual fee (for example, 0.8%–1.2% of the income base or account value).

- Optional benefit riders: Long‑term‑care style benefits, enhanced death benefits, or inflation riders may also have fees.

- Implicit costs: Limited upside (caps, participation, spreads) are part of how the insurer pays for guarantees.

- Surrender charges: Penalties if you take out more than the free allowance during the surrender period.

Surrender Periods and Liquidity

Most FIAs have surrender periods ranging from about 5 to 10+ years. During this time, you can usually withdraw a limited amount (often 10% per year) without a charge. Larger withdrawals may trigger surrender fees that decline over time according to the schedule in the contract.

Because of this, you should not put all your liquid savings into an annuity. Most retirees pair FIAs with other accounts that remain fully accessible for emergencies and big purchases.

Other Risks to Consider

- Inflation risk: If rates and crediting terms are low, your income may not keep pace with rising prices.

- Insurer credit risk: Guarantees depend on the claims‑paying ability of the insurance company.

- Complexity: Without guidance, it can be hard to compare products or understand the fine print.

- Tax penalties: Withdrawals before age 59½ can be subject to IRS penalties and income taxes for qualified accounts.

Where Fixed Indexed Annuities Fit in a Retirement Plan

Think of an FIA as one tool in a toolkit—not the entire toolbox. Many retirees blend FIAs with Social Security, pensions, CDs, bonds, and a prudent allocation to growth investments to balance safety, income, and long‑term opportunity.

When an FIA May Make Sense

- You want a portion of your income to be guaranteed for life.

- You are within 10–15 years of retirement or already retired.

- You have savings you do not plan to spend for several years.

- Market swings keep you up at night, but you still want some growth potential.

- You have at least 6–12 months of expenses in fully liquid savings outside the annuity.

When an FIA May Not Be a Fit

- You need full liquidity and may need to access most of the money within a few years.

- You are primarily seeking aggressive, stock‑like returns.

- You are uncomfortable committing to a multi‑year surrender schedule.

- You already have sufficient lifetime income from pensions and Social Security and value flexibility above all else.

- You do not fully understand how the contract works and do not want to take time to learn.

Clarity Corner

Common Myths About Fixed Indexed Annuities

Most TV personalities and naysayers on annuities refer to the variable annuity which we do not offer.

“My money is locked away forever.” — Most contracts allow annual penalty‑free withdrawals and provide liquidity at the end of the surrender period.

“I could lose everything if the market crashes.” — Market downturns do not directly reduce your contract value due to index performance when held under contract terms.

“They are always loaded with fees.” — Many basic FIAs have no explicit annual fee; costs can appear in riders and in the limits on upside growth.

Are fixed indexed annuities safe?

FIAs are generally considered conservative products, but they are not risk‑free. Your principal is protected from market losses when held under the terms of the contract. However, guarantees depend on the claims‑paying ability of the issuing insurer. You still face risks such as inflation, changes in crediting terms, and liquidity limits during the surrender period.

How are FIAs taxed?

Earnings inside an annuity grow tax‑deferred. For non‑qualified money (after‑tax savings), a portion of each withdrawal is typically treated as taxable earnings until all gains are withdrawn. For qualified money (IRAs, 401(k)s), distributions are generally taxed as ordinary income. Withdrawals before age 59½ may be subject to an additional 10% IRS penalty. Always consult a tax professional about your situation.

What happens to my annuity when I die?

Most FIAs allow you to name beneficiaries who can receive any remaining contract value when you pass away. In many cases, this can avoid probate. The specific options—lump sum, installments, or continuation of income—depend on the contract and on whether income payments have already begun.

Can I lose money in an FIA?

Market losses do not directly reduce your contract value due to index performance when the annuity is held under the terms of the contract. However, surrender charges, early withdrawal penalties, rider fees, or taxes can reduce the amount you receive if you take out money in ways the contract does not permit or if you exit early.

How do I compare different annuity offers?

Key items to compare include: the insurer’s financial strength ratings, the length and severity of the surrender schedule, crediting strategies and current rates (caps, participation, spreads), rider fees and guarantees, income payout options, and death benefit provisions. Working with an independent professional who can show side‑by‑side illustrations from multiple companies can make this easier.

Next Step

Get a Personalized Fixed Indexed Annuity Review

You deserve more than a generic sales pitch. In a short conversation, we can walk through your income needs, current accounts, and risk comfort—and show you how (or if) a fixed indexed annuity fits. If it is not right for you, we will say so.

- No obligation, no pressure—educational only.

- Weighed, side‑by‑side comparisons from multiple insurers.

- Plain‑English explanations tailored to your stage of life.

- Written summary of what we discuss so you can decide calmly.

Quick Intro Form

Tell us a bit about yourself and your retirement goals. We will reach out with a few time options for your Annuity Gal conversation.

Check out our Annuity Games under All Things Annuities. And Educate yourself at Annuity University.

Copyright © 2026 Annuity Gal LLC. All rights reserved.